Real estate is as yet a significant venture for Canadians despite rising home costs. Myriad home-purchasing plans were postponed due to the financial slump in the pandemic.

However, others had an ideal chance to make benefits out of lower interest rates, thanks to Covid relief policies.

The method involved with purchasing a home, regardless of whether it’s a completely separated house, apartment, or condominium, doesn’t begin when you call a real estate agent and mastermind a survey.

There are myriad facets you are supposed to attend!

In case you’ve never purchased a home before, how and where would you begin your journey to become a homeowner – well, we have formatted a bit-by-bit guide to visit you through all the important aspects of purchasing a home in Canada.

Ask Yourself before Buying your First Home

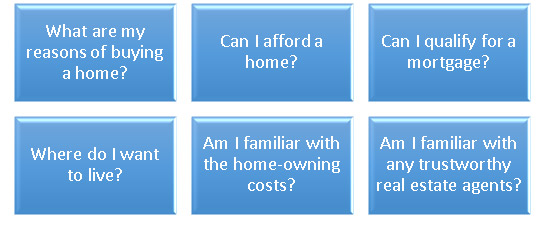

Answer these questions, to yourself, prior to getting into the home-purchasing procedures:

What are my reasons for buying a home?

There could be several reasons pushing you towards owning a house.

- Spending savings on a solid investment i.e. home

- Settle with family

- Give up on renting

- Pride of ownership

These can be some of the many reasons – clarifying your objective would help you prioritize and make mindful decisions.

Can I afford a home?

Some costs of buying a home could be:

- Bank appraisal costs

- Down payment

- Homeowners insurance

- Taxes

Since expenses are glued with making this investment, you would need to figure out the expenses and savings. You may hire a mortgage professional to give you an in-depth guide.

Your housing costs/ month should not be more than 32% of your gross household income per month as per Canada Mortgage and Housing Corporation.

Can I qualify for a mortgage?

An average Gucci purse costs $2,300. The reason for putting it like this is if you don’t qualify for a mortgage – you should stop hunting for a home and look for reasons behind this situation.

- Bankruptcies

- Low credit scores

- Late payments

- Poor employment history

These are some examples of potential mortgage disqualification grounds.

If you aspire of being a homeowner soon, resolve these obstacles and look for ways to improve credit scores for eased mortgage insurance rules in Canada.

Where do I want to live?

Location means your lifestyle choice and consequently its affordability. Planning of buying a home near the office or immediate family, take an estimation of purchasing costs there!

Am I familiar with the home-owning costs?

Purchasing a home is on one side, but owning a home has a cost too – and a homeowner cannot actually must not, skip that! You wouldn’t want to regret your purchasing decision later, right?

An estimation of annual home maintenance costs in Canada in about $5,800 annually.

These could be:

- General Maintenance

- Property Taxes

- Water, Internet, Gas

- Unexpected Repairs

- Bills

Am I familiar with any trustworthy real estate agents?

An experienced real estate agent who knows the local market, and is ready to address your wants and needs regarding home purchase can definitely reduce the confusion, frustration, and anxiety associated with the home buying journey.

You would need a real estate agent to save you some time and effort if you are an employee or run a business.

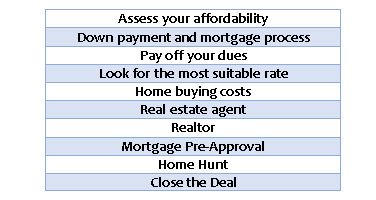

A Practical Guide to Help You Buy a House in Canada

ⱷ Assess Your Affordability

Know your budget. Analyze your savings and spending if you have not done it already. Mortgage costs and monthly salary ratio should also be kept under check.

- What is your household income after tax deduction?

- How much do you spend on household expenses, groceries, bills, gas, tuition, every month; on average?

- Now that you’ve analyzed your expenses and income – find ways you can make savings.

These savings can be utilized to clear/ pay off any debts if you own a secured credit card or unsecured credit card and other loans.

Homeownership and lifestyle expenses can be managed better once you know what you can afford!

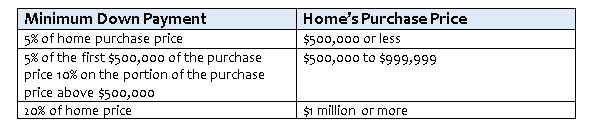

ⱷ Down Payment and Mortgage Process

To purchase a house, you should have your own money in addition to the loan/ mortgage options.

5% is the minimum amount of down payment if your potential home’s price is $500,000 or less.